Do you use PayPal, Cash App, Zelle, or Venmo to collect rent? If so, new rules mean that you could owe taxes on digital transactions. Beginning in 2022, the Internal […]

Did you miss our previous article…

https://diyinvestorresources.com/?p=622

Do you use PayPal, Cash App, Zelle, or Venmo to collect rent? If so, new rules mean that you could owe taxes on digital transactions. Beginning in 2022, the Internal […]

Did you miss our previous article…

https://diyinvestorresources.com/?p=622

We all know the old saying in real estate: “Location, location, location.” There are many factors that can contribute to a prime location—good schools, low crime rate, population increase, job […]

Did you miss our previous article…

https://diyinvestorresources.com/?p=602

Military members in the real estate community love to preach about how great the VA loans are for financing primary residences. They also love the fact that these primary residences […]

Did you miss our previous article…

https://diyinvestorresources.com/?p=596

401(k) plans can help you save for retirement in a significantly tax-advantaged way. However, the Internal Revenue Service (IRS) requires that you start taking withdrawals from their qualified retirement accounts when you reach the age 72. These withdrawals are called required minimum distributions (RMDs).

In exchange for the tax advantages you enjoy by contributing to your 401(k) plan, the IRS requests collection of taxes on these amounts when you turn 72. The IRS taxes RMDs as ordinary income, meaning withdrawals will count towards your total taxable income for the year.

Generally, the IRS collects taxes on the gains in retirement accounts such as 401(k)s. However, if Roth 401(k) account assets are held for at least 5 years, Roth 401(k) funds are not taxed. Because there are taxes being paid to the government, these distributions are NOT eligible for rollover to another account.

Before the 2019 SECURE Act, RMDs applied to employees who turned 70 ½. However, this legislation increased the RMD age to 72 starting in 2020.

You may remember that the CARES Act, passed in March 2020 in response to the COVID-19 crisis, temporarily waived RMDs for 2020. RMDs resumed for the 2021 plan year with the newly increased age limit of 72.

How much do I have to withdraw?

RMDs are calculated based on your age and your account balance as of the end of the previous year. To determine the required distribution amount, Betterment divides your previous year’s ending account balance by your life expectancy factor (based on your age) from the uniform lifetime table (shown below). As a note, if you had no balance at the end of the previous year, then your first RMD will not occur until the following year.

Uniform Lifetime TableAge of Plan ParticipantLife Expectancy (in Years)7027.47126.57225.67324.77423.87522.97622.07721.27820.37919.58018.78117.98217.18316.38415.58514.88614.18713.48812.78912.09011.49110.89210.2939.6949.1958.6968.1977.6987.1996.71006.31015.91025.51035.21044.91054.51064.21073.91083.71093.41103.11112.91122.61132.41142.1115 and older1.9

Additionally, if you have taken a cash distribution from your 401(k) account in any given year you are subject to an RMD, and that distribution amount is equal to or greater than the RMD amount, that distribution will qualify as the required amount and no additional distribution is required.

Turning 72 in a given year doesn’t mean that you have to take an RMD. Only those who turn 72 in a given year AND meet any of the following criteria must take an RMD:

You have taken an RMD in previous years. If so, then you must take an RMD by December 31 of every year.You own more than 5% of the company sponsoring the 401(k) plan. If so, then you must take an RMD by December 31 every year.You have left the company (terminated or retired) in the year you turned 72. If so, then the first RMD does not need to occur until April 1 (otherwise known as the Required Beginning Date) of the following year but must occur consecutively by December 31 for every year.>Example: John turned 72 on June 1, 2021. John also decided to leave his company on August 1, 2021. He has been continuously contributing to his 401(k) account for the past 5 years. The first RMD must occur by April 1, 2022. The next RMD must occur by December 31, 2022 and every year thereafter.>NOTE: that this criteria means that you do NOT need to take an RMD if you meet the RMD age and are still working.You are a beneficiary or alternate payee of an account holder who meets the above criteria.

Failure to take an RMD for a given year will result in a penalty of 50% of the amount not taken on time by the IRS.

Your employer will notify you that you may be subject to an RMD and provide you with an RMD form. You will need to fill and return this form to your employer for approval. Betterment will process the RMD and the distribution will be delivered via the method of your choice (check or ACH).

Want a better 401(k)?

Learn More>

Did you miss our previous article…

https://diyinvestorresources.com/?p=586

Today, we are excited to announce that we will begin integrating the $VOTE ETF, recently launched by Engine No. 1, into all of Betterment’s Socially Responsible Investing portfolios.

This new ETF invests in 500 of the largest U.S. companies, weighted according to their size, with a management fee of only .05%. You might think that this sounds a lot like a garden variety index fund tracking the S&P 500—a commodity for many years now.

So, why the excitement?

In short, $VOTE represents a highly innovative approach to pushing the economy towards sustainability via index fund investing. It may be “passive” in the traditional sense—buying shares in companies purely based on an index—but it is “active” when it comes to engaging with those companies as a shareholder.

Historically, values-aligned investing has often been synonymous with avoiding the purchase of certain stocks—a practice often referred to as “divestment.” The alternative to divestment is “engagement.” By owning a stock, and using your rights to vote on shareholder resolutions, you can attempt to change the company’s activities from the inside.

Vanguard, BlackRock, and State Street—the “Big Three” largest fund managers—are collectively the biggest shareholders in most companies, but have historically been reluctant to rock the boat and aggressively challenge management. As a result, when it comes to investing through index funds, the full potential of shareholder engagement to drive change hasn’t been tapped.

Engine No. 1’s new $VOTE ETF promises to change that. To understand why, it helps to understand the mechanics of how shareholders can push for change.

Purchasing stock in a company grants you not just a share of its profits, but also the right to influence its decision-making. This process is called “proxy voting,” which can be a powerful tool with the potential to transform the entire economy, company by company.

Publicly traded companies operate like quasi-democracies, accountable to their shareholders. They hold annual meetings, where shareholders can vote on a number of topics. Shareholders who disagree with some aspect of how a company’s business is conducted can engage with management, and if they feel they aren’t being heard, can present an alternate course of action by making a “shareholder proposal.”

If they can persuade a majority of all shareholders to vote in support of the proposal, they can overrule management. When more drastic change is warranted, such “activist” shareholders can seek to replace management entirely, by nominating their own candidates for the company’s board of directors.

Social change via shareholder activism has a storied history. As early as 1951, in a seminal case, civil rights leader James Peck took the fight to the proxy arena, by filing a shareholder proposal with the Greyhound Corporation, recommending that the bus operator abolish segregated seating in the South.

Seventy years later, on May 26, 2021, activist hedge fund Engine No. 1 stunned the corporate world by winning a proxy battle against the current leadership of ExxonMobil, persuading a coalition of shareholders to elect three of its own candidates to the board—the first ever climate-centered case for change.

Engine No. 1 argued that Exxon’s share price was underperforming that of its peers because the company was unprepared for the transition away from fossil fuels. It nominated candidates for the board that would push the oil giant to embrace renewable energy. Against all odds, holding just .02% of Exxon’s stock, Engine No. 1 prevailed.

Corporate boardrooms across the entire S&P 500 are buzzing, asking what the Exxon coup means for them. Where will environmentally and socially conscious investors strike next? These questions are warranted: The Exxon campaign was a first, but it surely won’t be the last.

Individual investors are increasingly aware of proxy voting as a domain by which their portfolios can channel their values. In a recent Morningstar report, 61% of those surveyed said that sustainability should be factored into how votes attributable to their 401(k)s are cast.

However, most Americans, including Betterment customers, don’t buy stock of companies like Greyhound or Exxon directly, but through index funds.

When you buy a share of an index fund, the index fund manager uses your money to buy stocks of companies on your behalf. As a shareholder of the fund, you benefit financially when these underlying stocks rise in value, but the index fund is technically the shareholder of each individual company, and holds the right to participate in each company’s proxy voting process.

As more investors tell the industry that they want their dollars to advance sustainable business practices, the Big Three have been feeling the pressure to work these preferences into their proxy voting practices.

This year, they are showing some signs of change. Notably, the Big Three ultimately joined Engine No. 1’s coalition, which could not have prevailed against Exxon without their support. However, even if the Big Three, who manage trillions on behalf of individual investors, continue to side with the activists, what’s missing is a way for individuals to invest their dollars not just to support these campaigns, but to spearhead them as well.

Activist shareholder campaigns are generally led by hedge funds, and what happened with Exxon was no exception. However, by launching an ETF that anyone can invest in, Engine No. 1 is looking to break that mold.

In 2020, investors poured $50 billion into sustainable index funds—double that of 2019, and ten times that of 2018. The $VOTE ETF should bring even more investors off the sidelines, and into sustainable investing, for two reasons.

First, rather than dilute its efforts, $VOTE intends to spearhead a handful of campaigns, pushing companies to improve their environmental and social practices. A focus on the highest impact, and most powerful narratives, will continue to raise awareness for the power of shareholder activism.

Second, $VOTE is designed for mass adoption, not as a niche strategy. With a management fee of only .05%, and tracking a market cap weighted index, $VOTE is designed to ensure no trade-off to long-term returns. It is also well-suited for those investing for retirement—and as of today, it will make its way into its first ever 401(k) plan, via Betterment for Business.

We know that many of our customers want to invest for real impact, especially if they can do so without sacrificing their long-term financial goals. If you’re investing through any of Betterment’s three Socially Responsible Investing portfolios, $VOTE will have a target weight equal to 10% of your exposure to the U.S. stocks.

With $VOTE in your portfolio, you’ll know that your dollars are directly supporting whatever engagements Engine No. 1 launches next. As their subsequent work unfolds, we will be monitoring their efforts, and updating our customers on the impact their investments are driving.

Now that $VOTE exists, anyone—not just Betterment customers—can invest in it, which is a great thing. The bigger it gets, the more it can drive change, and you, as an investor, get to help write the next chapter.

Invest for better

Join Betterment>

Along with RIA in a Box®, RightCapital, and Wealthbox, Betterment for Advisors is excited to introduce the RIA Tech Suite a set of services and tools that advisors can use to help automate and streamline back-office tasks.

Together, these intuitive and complementary tech tools can streamline everyday practice management, giving you more time to acquire new business and to provide a better experience for your current clients.

Additionally, the RIA Tech Suite includes discounted pricing for firms that adopt two or more of the services — a discount that can save an average RIA firm up to $3,100 in their first year.

Here are the tools available on the RIA Tech Suite:

Betterment for Advisors – A leading digital-first wealth management platform that leverages smart-tax technology.RIA in a Box® – Compliance, cybersecurity, and operational software for investment advisors.RightCapital – Wealth planning software that makes planning easier and more powerful for advisors and their clients.Wealthbox – A leading CRM software application that helps advisors manage their clients and collaborate with their team.

The RIA Tech Suite can foster growth for tech-centric firms that are focused on efficient client service and expanding their books of business.

“Our goal at Betterment for Advisors is to empower advisors to grow their businesses and build deeper client relationships,” writes Jon Mauney, General Manager of Betterment for Advisors. “The four companies that are part of the RIA Tech Suite all share this objective with a common approach to their services: providing beautifully designed, easy-to-use, and powerful tools for advisors and their clients.”

ny links provided to other websites are offered as a matter of convenience and are not intended to imply that Betterment or its authors endorse, sponsor, promote, and/or are affiliated with the owners of or participants in those sites, unless stated otherwise.

Did you miss our previous article…

https://diyinvestorresources.com/?p=579

Money and emotions have long gone hand-in-hand, and this is no more apparent than during significant financial crises. From the 2008 market crash to COVID-19’s economic impact, we’ve seen first hand how money has the ability to impact our stress levels, mental health and personal relationships. And yet in times of particular financial strife—or likely because of it— many people take actions with their money that often undermine their emotional wellbeing, sacrificing long-term happiness for short-term pleasure without even realizing it at the time.

This trend toward short-termism grew in 2020: people stuck inside, on screens all day and kept from their normal activities sought new ways to fill their time and energy. Many took up day trading, culminating in one of the wildest rides at the beginning of 2021 (and recent surges demonstrating people are still trying to head to the moon) with Gamestop, AMC, Blackberry and other retail stocks caught in the middle of a clash between amateur retail and institutional investors.

Following this eventful start to the year, Betterment was curious to see both the immediate and long-term impact this had on investors, particularly those involved in the action. In this report — a survey of 1,500 active investors conducted by a third party — we took a look at the rise of day trading activity and the impact it did (or didn’t have) on people’s behavior. From their own forecasts, it looks like “the rise of the day trader” is here to stay — but forecasting is hard. None of us would have bet on the pandemic and the changes it’s causing. People actually aren’t very good at forecasting their own preferences and behavior in the future, so it will be interesting to see if said forecasts actually come to fruition.

Regardless, at Betterment we welcome the addition of consumers looking to learn more about the markets and, ultimately, how to balance their portfolios for the long-term too.

With movie theaters, stadiums, bars and restaurants closed, many people took up day trading during the COVID-19 pandemic. Half of our total respondents said they actively day trade investments, and nearly half of those day-traders (49%) have been doing it for 2 years or less.

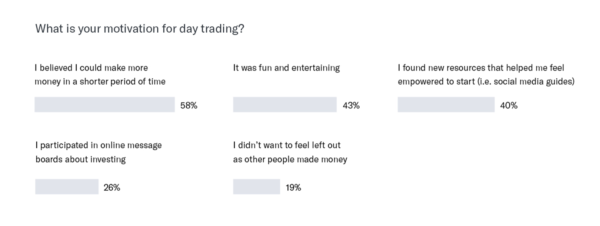

While most day traders indicated their main reason for doing so was that they believed they could make more money in a shorter period of time (58%), many (43%) also indicated it was because it is fun and entertaining. Of those who look to day trading for fun/entertainment, half (52%) said it was to make up for the bulk of their other hobbies—like sports, live music, social gatherings, gambling—not being available due to COVID-19.

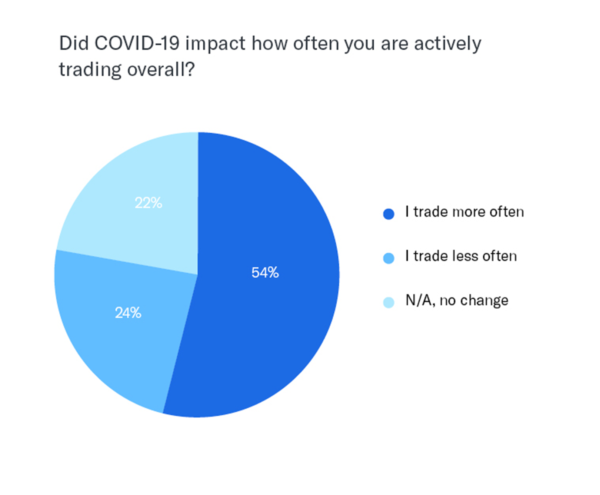

And these day traders have fully acknowledge that COVID-19 played a big impact role in their market activity overall: 54% indicated they trade more often as a result of COVID-19; and interestingly, 58% said they expect to day trade more as normal activities return and COVID-19 restrictions are lifted, likely as a result of what they learned during this downtime. Only 12% said they expect to trade less.

More than half (58%) are using less than 30% of their portfolio to actively trade individual securities or stocks. Nearly two thirds also allow an advisor (either online or in-person) to manage a separate part of their portfolio.

Betterment’s Point Of View:It is interesting to see more respondents expect to day trade more after the pandemic than are currently day trading: we imagine it is hard for people to forecast themselves into the future and imagine doing things differently than they are now. However, what is positive to see is these people aren’t using an excessive amount of their portfolio to day trade. The majority of investors day trade with a minority of their total investing balance, and delegate day-to-day management of the larger portion of their portfolio to an advisor.

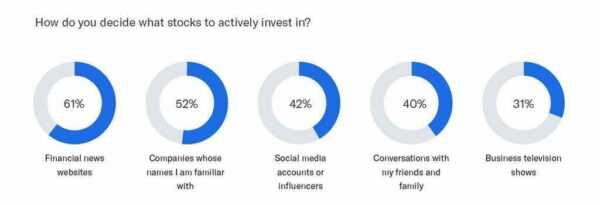

Passing hobby or not, how educated is the average day trader on what they’re buying and what they stand to gain—or lose? Sixty one percent rely on financial news websites to decide which stocks to buy, but nearly half (42%) are influenced by social media accounts, showing just how powerful “memestocks” can be.

Betterment’s Point Of View:More than half of the respondents suggested they buy stocks based on company names they’re familiar with, but we’ve seen this lead to issues in the past—with “ticker mis-matches,” where people trade the ticker of a stock that isn’t the correct company. For example, after a tweet from Elon Musk about Signal (a non-profit messaging app), a different company’s stock was sent soaring 3,092%.

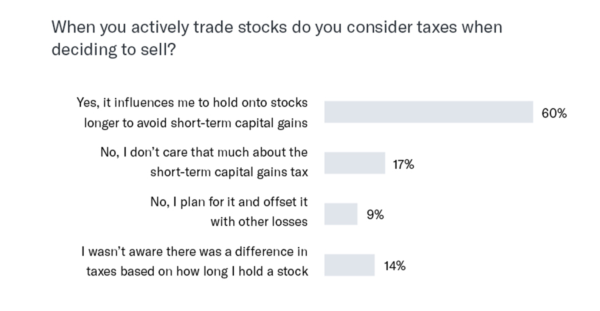

We also asked day trader respondents if they consider capital gains taxes when deciding to sell their investments. While the majority (60%) indicated that it influences them to hold onto stocks longer to avoid short-term capital gains, 14% said they weren’t aware there was a difference in taxes based on how long they hold a stock. Another 17% said they simply don’t care about the short-term capital gains tax.

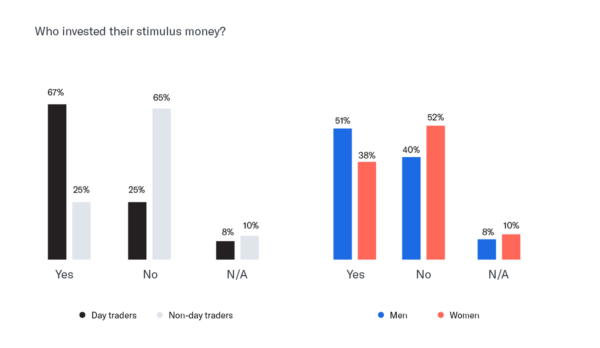

Almost all (91%) respondents received some stimulus money, and nearly half (46%) invested some of that money; of those who did invest it, 70% invested half or less of their stimulus. Day trader and male respondents were more likely to invest then their counterparts, as represented in the graphic below.

This is in contrast to our COVID-19 investor sentiment survey from 2020, where only 9% of respondents indicated they put some of their stimulus money towards investment. Last year’s response pool was primarily focused on building out their emergency funds, with 40% putting money into a safety net. This is a good indication that respondents are more comfortable with their financial situations this year, compared to the throes of the pandemic.

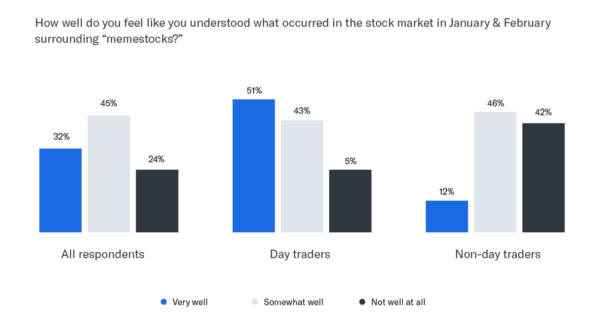

We asked all respondents how well they understood what occurred in the stock market in January & February surrounding “memestocks” like GameStop, AMC, BlackBerry and other retail investments.

Most indicated having some level of understanding, but nearly a quarter (24%) of all respondents said they didn’t understand it well at all; and only half (51%) of day trader respondents said they understood what happened very well.

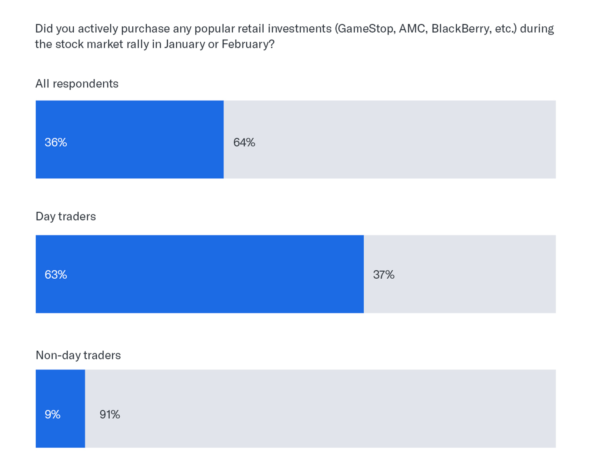

Nearly two-thirds (64%) of all survey respondents said they did not actively purchase any popular retail investments (GameStop, AMC, BlackBerry, etc.) during the stock market rally in January or February. But those that DID were primarily day traders.

Of all respondents that did buy in actively, 55% are still holding onto all their investments. Only 2% of those that sold these investments sold everything at a loss; 44% sold all for a profit and 54% sold some at a profit and some at a loss.

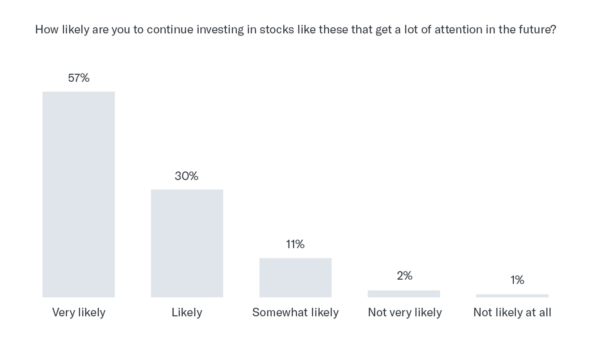

Of those that bought into memestocks, there is a near universal consensus that they will continue investing in stocks like these that get a lot of attention in the future—97% said they’re at least somewhat likely to invest.

Betterment’s Point Of View:It is interesting to see the majority of respondents holding onto their investments – are they expecting another high or holding on because they don’t want to admit they made a bad investment? Disposition Effect says people tend to hold on until they get back to zero loss; but seeing so few sell entirely for a loss is encouraging. However, 60% previously said thinking of short-term capital gains taxes encourages them to hold onto their investments longer, which is good to see.

It’s no secret that money and stress are linked, so we wanted to take a look at respondents’ money habits and how that may be impacting stress levels. The consensus is that for better and for worse day traders and younger generations are more engaged with their finances.

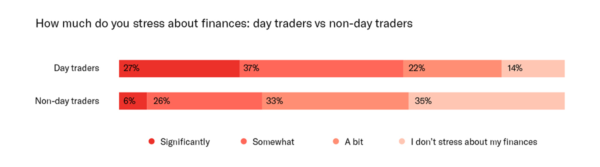

We asked respondents how much they stress about their finances on a daily basis—three quarters said they stress to some degree. Interestingly, when we looked a layer deeper, day traders are much more stressed than non-day trader—86% indicated they stress to some degree, vs 65% of their counterparts.

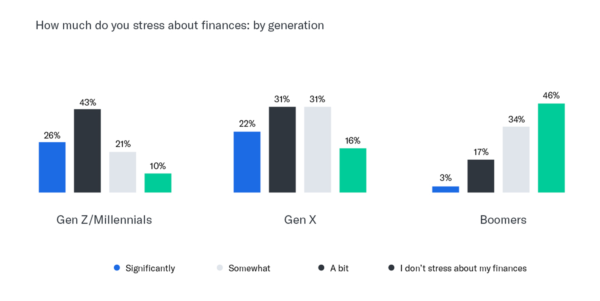

Unsurprisingly, younger generations are more stressed about their finances than older ones.

In looking at the causes of the stress: respondents are nearly equally concerned about money in the short term, near term future, and long term future with the top 3 financial stress factors being their daily expenses (43%), how much money they will have in retirement (43%), and how much money they have saved (42%).

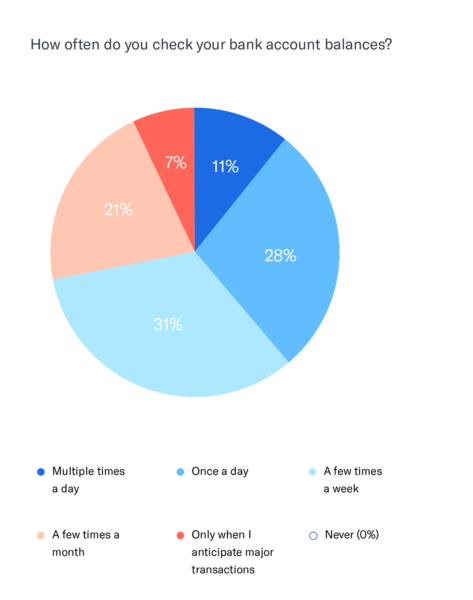

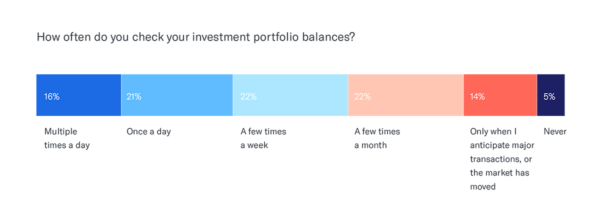

We asked respondents how often they are checking their bank account and investment portfolio balances – 39% are looking at their bank account balances every day, with 11% of those checking multiple times a day; 37% also check their investment portfolio balances every day, with 16% of those checking multiple times a day.

When we look a layer deeper, we find that day traders are checking both their bank account and investment portfolio balances significantly more than non-day traders.

50% of day traders indicated they check at least once a day (18% multiple times) vs 29% of non-daytraders (5% multiple times).Men check their accounts more often—41% at least once a day (13% multiple times) vs 36% of women (8% multiple times).46% of Gen Z/Millennials and Gen X both said they check their accounts at least once a day, whereas only 28% of Boomers said the same.Those making more money actually check their accounts more often—42% respondents making $100K or more check every day, compared to 39% of those making between $50-100K and 35% of those making less than $50K.

Unsurprisingly, 56% of day traders said they check their investment portfolio balances every day (25% multiple times a day), whereas only 18% of non-day traders said the same.41% of men check every day, compared to 30% of women.47% of Gen Z/Millennials check every day, compared to 41% of Gen X and 22% of Boomers.42% of those making 100K or more check every day, compared to 35% making between $50-100K and 30% of those making less than $50K.

Betterment’s Point Of View:The differences between men and women here are in line with research we’ve seen elsewhere. Women are less focused on market performance, and more focused on the end financial outcome. They also tend to invest at lower risk levels, so are less likely to see extreme ups and downs. Additionally, Women tend to be less competitive/score based in general, so are less interested in monitoring the game.

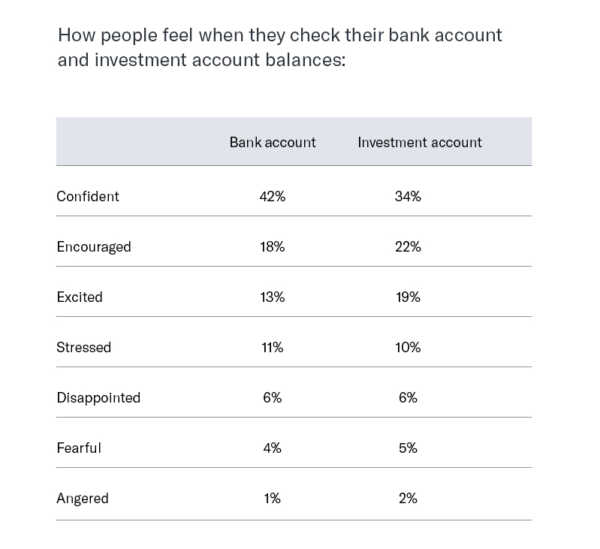

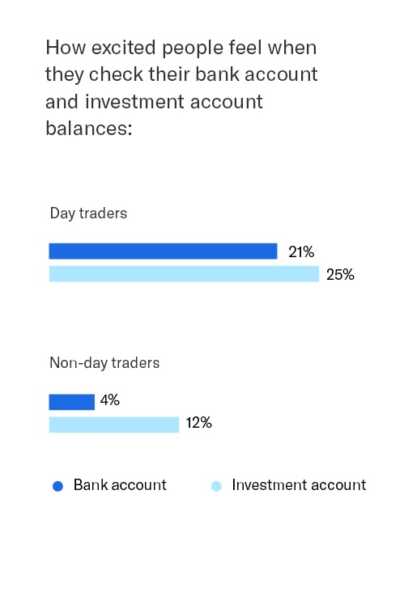

Encouragingly, when we asked people how they felt checking these accounts, the positive responses outweighed negative options for both. Interestingly, day traders were significantly more excited for both (21% for bank accounts, 25% for investments) than non-day traders (4% and 12%, respectively) as well.

Most respondents (89%) indicated they’re putting some money away every month, but it’s equally split as to where that money is actually going.

At Betterment, we have often compared day trading to going to Vegas—have a great time, enjoy yourself, but be prepared to come back home with fewer dollars in your wallet and a hangover. The trends outlined in this report seem to indicate that more people are dipping their toe into the investing pool and (so far) few have decided to walk away. Whether this trend will continue—and the long term impact it will have on people’s finances, health, stress, etc.—remains to be seen.

And for those who want to avoid the FOMO of the next big memestock, but aren’t sure of the best way to get started—a simple alternative is investing in a well diversified portfolio. That way, whenever someone asks if you own the hottest thing, you can say “yes”, regardless of what it is.

An online survey was conducted with a panel of potential respondents from April 26, 2021 to May 3, 2021. The survey was completed by a total of 1,500 respondents who are 18 years and older and have any kind of investment (excluded if only 401k). Of the 1,500 respondents, 750 of them actively day traded their investments while the other 750 did not. The sample was provided by Market Cube, a research panel company. All respondents were invited to take the survey via an email invitation. Panel respondents were incentivized to participate via the panel’s established points program, regardless of positive or negative feedback. Participants were not required to be Betterment clients to participate.

Findings and analysis are presented for informational purposes only and are not intended to be investment advice, nor is this indicative of client sentiment or experience.

Any links provided to other websites are offered as a matter of convenience and are not intended to imply that Betterment or its authors endorse, sponsor, promote, and/or are affiliated with the owners of or participants in those sites, unless stated otherwise.

Did you miss our previous article…

https://diyinvestorresources.com/?p=559

“Your 401(k) plan failed.” Those words can strike fear in the hearts of even the most seasoned business owners. However, there’s a way to avoid the stress of your plan’s annual nondiscrimination testing. By setting up a safe harbor 401(k), you can bypass some of the tests, such as the ADP and ACP tests, and focus on helping your employees save for their financial futures. But is a safe harbor 401(k) right for your company? Read on for answers to frequently asked questions about safe harbor 401(k) plans.

Before we explore safe harbor plans, let’s talk about nondiscrimination tests. Mandated by ERISA, these annual tests help ensure that 401(k) plans benefit all employees—not just business owners or highly compensated employees (HCEs). Because the government provides significant tax benefits through 401(k) plans, it wants to ensure that these perks don’t disproportionately favor high earners.

The three main nondiscrimination tests are:

Actual deferral percentage (ADP) test—Compares the average salary deferrals of HCEs to those of non-highly compensated employees (NHCEs).Actual contribution percentage (ADC) test—Compares the average employer contributions received by HCEs and NHCEs.Top-heavy test—Evaluates whether a plan is top-heavy, that is, if the total value of the plan accounts of “key employees” is more than 60% of the value of all plan assets. (IRS defines a key employee as an officer making more than $185,000, an owner of more than 5% of the business, or an owner of more than 1% of the business who made more than $150,000 during the plan year.]

It’s actually easier for large companies to pass the tests because they have many employees at varying income levels contributing to the plan. However, small and mid-size businesses may struggle to pass if they have a relatively high number of HCEs. If HCEs contribute a lot to the plan, but NHCEs don’t, there’s a chance that the 401(k) plan will not pass nondiscrimination testing.

So, you may be wondering: “What happens if my plan fails?” Well, you’ll need to fix the imbalance by returning 401(k) plan contributions to your HCEs or by increasing contributions to your NHCEs. If you have to refund contributions, affected employees may fall behind on their retirement savings—and that money may be subject to state and federal taxes! If you don’t correct the issue in a timely manner, there could also be a 10% penalty fee and other serious ramifications.

If you offer employees a safe harbor 401(k) plan, you can avoid these time-consuming, headache-inducing compliance tests.

So, let’s back up for a minute. What exactly is a safe harbor 401(k) plan? Put simply, it’s a defined contribution retirement plan that’s exempt from nondiscrimination testing. It’s like a typical 401(k) plan except it requires you to contribute to the plan on your employees’ behalf, sometimes as an incentive for them to save in the plan. This mandatory employer contribution must vest immediately—rather than on a graded or cliff vesting schedule. This means your employees can take these contributions with them when they leave, no matter how long they’ve worked for the company.

To fulfill safe harbor requirements, you can elect one of the following general contribution formulas:

Basic safe harbor match—Employer matches 100% of employee contributions, up to 3% of their compensation, plus 50% of the next 2% of their compensation.Enhanced safe harbor match—Employer matches 100% of employee contributions, up to 4% of their compensation.Non-elective contribution—Employer contributes 3% of each employee’s compensation, regardless of whether they make their own contributions.

These are only the minimum contributions. You can always increase non-elective or matching contributions to help your employees on the road to retirement.

At the end of the day, you want your employees to achieve the retirement they envision—and a safe harbor 401(k) plan can help them pursue it (while saving you time and effort). Consider these top five reasons to elect a safe harbor 401(k) plan:

1. Attract and retain top talent—Offering your employees a matching or non-elective contribution is a powerful recruitment tool. In fact, a Betterment for Business study found that nearly half of respondents said a company match was a factor in whether or not they accepted a new job. Plus, an employer contribution is a great way to reward your current employees (and incentivize them to save for their future).

2. Improve financial wellness—Studies show that financial stress impacts employees’ ability to focus on work. By helping your employees save for retirement, you help ease that burden and potentially improve your company’s productivity and profitability.

3. Save time and stress—Administering your 401(k) plan takes time—and it can become even more time-consuming and stressful if you’re worried that your plan may not pass nondiscrimination testing. Skip the tests altogether by electing a safe harbor 401(k).

4. Reward your top earners—With a safe harbor 401(k) plan, you can ensure that you and your HCEs will be able to max out your retirement contributions (without the fear that contributions will be returned if the plan fails nondiscrimination testing).

5. Reduce your taxable income—Like any employer contribution, safe harbor contributions are tax deductible! Plus, you can receive valuable tax credits to help offset the costs of your 401(k) plan.

n ideal solution for small businesses

If you’ve failed nondiscrimination testing in the past—or are concerned that your lower earning employees won’t participate in a 401(k) plan—a safe harbor plan may be the best solution for your small business.

Get a safe harbor 401(k) plan that works for you and your employees. Start now.

The main consideration is that safe harbor contributions could increase your overall payroll by 3% or more depending upon your participation rates and contribution formula. Therefore, it’s important to think about whether your company has the financial capacity to make employer contributions on an annual basis.

The good news is that 401(k) plans—including those with safe harbor provisions—are more affordable than they have been in the past. In fact, providers like Betterment now offer comprehensive plan solutions at low costs. Learn more now.

If you’re thinking about setting up a safe harbor plan or adding a safe harbor match to your existing plan, here are a few safe harbor 401(k) rules you need to know:

Starting a new plan—For calendar year plans, October 1 is the final deadline for starting a new safe harbor 401(k) plan. But don’t cut it too close—you’re required to notify your employees 30 days before the plan starts. So, if you’re mulling over a safe harbor plan, be sure to talk to your plan provider well in advance.Adding a safe harbor match to an existing plan—If you want to add a safe harbor match provision to your current plan, you can include a plan amendment that goes into effect January 1. However, employees are required to receive a notice at least 30 days prior.Adding a safe harbor nonelective contribution to an existing plan—Thanks to the SECURE Act, plans that want to become a nonelective safe harbor plan have newfound flexibility. An existing plan can implement a 3% nonelective safe harbor provision for the current plan year if amended 30 days before the close of the plan year. Plans that decide to implement a nonelective safe harbor contribution of 4% or more have until the end of the following year in which the plan will become a safe harbor. Importantly, the SECURE Act eliminated the usual employee notice requirement for nonelective safe harbor plans.Communicating with employees—Every year, eligible employees need to be notified about their rights and obligations under your safe harbor plan (except for those with nonelective contributions, as noted in the previous bullet). Notice must be given at least 30 days, but no more than 90 days, before the beginning of the plan year. Want to learn more about notices? Visit the IRS website.A plan provider like Betterment will be able to assist you with everything you need to create the safe harbor 401(k) plan that’s right for your company.

When it comes to choosing the right provider, it’s all about asking the right questions. Here’s how Betterment would answer them:

Do you have experience setting up safe harbor 401(k) plans?

Our team has significant experience working with safe harbor 401(k) plans. We help you understand each step of the onboarding process so you can start your plan quickly and easily. Plus, we have the expertise you need to handle every detail—from safe harbor 401(k) eligibility rules to investment options.How much does your service cost?

Our fees are a fraction of the cost of most providers. Plus, we’re always fully transparent about fees so there are no surprises for you or your employees.How easy will it be for me to administer our plan on an ongoing basis?

Our intuitive platform works to reduce your administrative burden. That means you’ll stay informed of what you need to do and when you need to do it—simplifying plan administration.Do you offer financial wellness support for employees?

Our high-tech solution enables us to give employees holistic, personalized advice on everything from contribution rates to investments. Plus, we can link employees’ outside investments, savings accounts, IRAs, and spousal/partner assets, so they can get a big picture view of their long- and short-term financial goals.

If you are looking to implement a safe harbor plan for the 2021 plan year, it must be live by October 1, 2021. Sign up with Betterment by August 2, 2021 to start reaping the benefits of a safe harbor plan this plan year!

Want to continue the conversation?

Let’s talk.>

Betterment is not a tax advisor. Please consult a qualified tax professional.

Did you miss our previous article…

https://diyinvestorresources.com/?p=557

By state law, businesses with 50 or more employees in California must provide a retirement program to their employees by June 30, 2021. And employers with five or more employees must provide a program by June 30, 2022.

If you’re an employer in California, you must offer the CalSavers Retirement Savings Program—or another retirement plan such as a 401(k). Faced with this decision, you may be asking yourself: Which is the best plan for my employees?

To help you make an informed decision, we’ve provided answers to frequently asked questions about CalSavers:

No. California laws require businesses with 50 or employees to offer retirement benefits, but you don’t have to elect CalSavers. If you provide a 401(k) plan (or another type of employer-sponsored retirement program), you may request an exemption.

CalSavers is a Payroll Deduction IRA program—also known as an “Auto IRA” plan. Under an Auto IRA plan, if you don’t offer a retirement plan, you must automatically enroll your employees into a state IRA savings program. Specifically, the CalSavers plan requires employers with at least five employees to automatically enroll employees at a 5% deferral rate with automatic annual increases, up to a maximum of 8%.

As an eligible employer, you must withhold the appropriate percentage of employees’ wages and deposit it into the CalSavers Roth IRA on their behalf. Employees retain control over their Roth IRA and can customize their account by selecting their own contribution rate and investments—or by opting out altogether.

CalSavers is a simple, straightforward way to help your employees save for retirement. CalSavers is administered by a private-sector financial services firm and overseen by a public board chaired by the State Treasurer. As an employer, your role is limited to uploading employee information to CalSavers and submitting employee contributions via payroll deduction. Plus, there are no fees for employers to offer CalSavers, and employers are not fiduciaries of the program.

Yes, there are factors that may make CalSavers less appealing than other retirement plans. Here are some important considerations:

CalSavers is a Roth IRA, which means it has income limits—If your employees earn above a certain threshold, they will not be able to participate in CalSavers. For example, single filers with modified adjusted gross incomes of more than $140,000 would not be eligible to contribute. If they mistakenly contribute to CalSavers—and then find out they’re ineligible—they must correct their error or potentially face taxes and penalties. However, 401(k) plans aren’t subject to the same income restrictions.CalSavers is not subject to worker protections under ERISA—Other tax-qualified retirement savings plans—such as 401(k) plans—are subject to ERISA, a federal law that requires fiduciary oversight of retirement plans.Employees don’t receive a tax benefit for their savings in the year they make contributions—Unlike a 401(k) plan—which allows both before-tax and after-tax contributions—CalSavers only offers after-tax contributions to a Roth IRA. Investment earnings within a Roth IRA are tax-deferred until withdrawn and may eventually be tax-free.Contribution limits are far lower—Employees may save up to $6,000 in an IRA in 2021 ($7,000 if they’re age 50 or older), while in a 401(k) plan employees may save up to $19,500 in 2021 ($26,000 if they’re age 50 or older). So even if employees max out their contribution to CalSavers, they may still fall short of the amount of money they’ll likely need to achieve a financially secure retirement.No employer matching and/or profit sharing contributions—Employer contributions are a major incentive for employees to save for their future. 401(k) plans allow you the flexibility of offering employer contributions; however, CalSaver does not.Limited investment options—CalSavers offers a relatively limited selection of investments, which may not be appropriate for all investors. Typical 401(k) plans offer a much broader range of investment options and often additional resources such as managed accounts and personalized advice.Potentially higher fees for employees—There is no cost to employers to offer CalSavers; however, employees do pay $0.83-$0.95 per year for every $100 in their account, depending upon their investments. While different 401(k) plans charge different fees, some plans have far lower employee fees. Fees are a big consideration because they can seriously erode employee savings over time.

For many employers —even very small businesses—a 401(k) plan may be a more attractive option for a variety of reasons. As an employer, you have greater flexibility and control over your plan service provider, investments, and features so you can tailor the plan that best meets your company’s needs and objectives. Plus, you’ll benefit from:

Tax credits—Thanks to the SECURE Act, you can now receive up to $15,000 in tax credits to help defray the start-up costs of your 401(k) plan. Plus, if you add an eligible automatic enrollment feature, you could earn an additional $1,500 in tax credits.Tax deductions—If you pay for plan expenses like administrative fees, you may be able to claim them as a business tax deduction.

With a 401(k) plan, your employees may also likely have greater:

Choice—You can give employees, regardless of income, the choice of reducing their taxable income now by making pre-tax contributions or making after-tax contributions (or both!) Not only that, but employees can contribute to a 401(k) plan and an IRA if they wish—giving them even more opportunity to save for the future they envision.Saving power—Thanks to the higher contributions limits of a 401(k) plan, employees can save thousands of dollars more—potentially setting them up for a more secure future. Plus, if the 401(k) plan fees are lower than what an individual might have to pay with CalSavers, that means more employer savings are available for account growth.Investment freedom—Employees may be able to access more investment options and the guidance they need to invest with confidence. Case in point: Betterment offers 500+ low-cost, globally diversified portfolios (including those focused on making a positive impact on the climate and society).Support—401(k) providers often provide a greater degree of support, such as educational resources on a wide range of topics. For example, Betterment offers personalized, “always-on” advice to help your employees reach their retirement goals and pursue overall financial wellness. Plus, we provide an integrated view of your employees’ outside assets so they can see their full financial picture—and track their progress toward all their savings goals.

The state will notify you of your company’s non-compliance. Ninety days after the notification, if you still fail to comply, there is a penalty of $250 per eligible employee. If non-compliance extends 180 days or more, there is an additional penalty per eligible employee. As you can imagine, your company could end up paying thousands of dollars in fees for non-compliance!

If you decide that CalSavers is most appropriate for your company, visit the CalSavers website to register before:

June 30, 2021 – for businesses with 50+ employees in CaliforniaJune 30, 2022 – for businesses with 5+ employees in California

If you decide to explore your retirement plan alternatives, talk to Betterment. We can help you get your plan up and running fast—and make ongoing plan administration a breeze. Plus, our fees are well below industry average. That can mean more value for your company—and more savings for your employees. Get started now.

Betterment is not a tax advisor, and the information contained in this article is for informational purposes only.

Want a better 401(k)?

Learn More>

Your water heater fails. Your car breaks down on the side of the road. Your spouse loses their job because of a global pandemic. Life is filled with challenges, and some are more stressful and expensive than others. As a small business owner, you’ve likely witnessed firsthand how financial emergencies can impact your employees. Not only does the stress affect employees’ personal lives, it can also affect their work performance, attendance, and focus.

That’s why an emergency fund —with enough money to cover at least a few months of expenses—is such an important part of your employees’ overall financial plan. However, many people lack this critical safety net.

According to research by the Employee Benefit Research Institute (EBRI), half of workers say they have a rainy day fund that could cover three months of expenses in the case of sickness, job loss, economic downturn, or another emergency. However, only one in five families actually has liquid savings of more than three months of income. Notably, EBRI found that the lack of an emergency savings fund was not limited to just younger employees or those with lower incomes—it’s an issue that transcends age and income.

When faced with an emergency, employees without a financial safety net may turn to credit cards, take a payday loan, or even raid their retirement savings—triggering early withdrawal penalties and derailing their retirement savings progress. Having a solid emergency fund can help prevent employees from spiraling into a difficult financial predicament with wide-reaching implications. Craig Copeland, Senior Research Associate at EBRI, explains, “Given the low percentage of workers and families who have sufficient savings to cover a loss of income for any extended period, emergency savings programs could be directly beneficial to workers and indirectly beneficial to employers through higher employee satisfaction.” In fact, more employers than ever are encouraging their employees to save for unexpected financial emergencies.

So, what should your employees consider when setting up an emergency fund? At Betterment, we recommend:

Saving at least three to four months of expenses—If employees have a financial safety net, they’ll feel more confident focusing on other important goals like retirement or home ownership.Investing emergency fund money—By investing their money—not socking it away in a low-interest savings account—employees don’t run the risk of losing buying power over time because of inflation. In fact, our current recommended allocation for an emergency fund is 30% stocks and 70% bonds.Making it automatic—Setting up a regular, automatic deposit can help employees stick to their savings plan because it reduces the effort required to set aside money in the first place.

With an emergency fund, your employees have the peace of mind of knowing that they have a financial cushion in the case they need it now or in the future.

Some employees may feel like they have to choose between building their emergency fund and saving in their workplace retirement plan. But it doesn’t have to be a choice. With the right 401(k) plan provider, your employees can save for retirement and build an emergency fund at the same time. For example, the Betterment platform is “more than just a 401(k) in that it provides:

Quick and easy emergency saving fund set-up

Betterment makes it easy to establish an emergency savings fund—helping ensure employees don’t need to dip into their 401(k) when faced with unexpected financial difficulties. If your employees aren’t sure how much to save, Betterment can calculate it for them using their gross income, zip code, and research from the American Economic Association and the National Bureau of Economic Research.Betterment will also estimate how much employees need to save to build the emergency fund they want to reach their target amount in their desired time horizon. Using our goals forecaster, employees can model how much they need to save each month to reach their emergency fund goal and view different what-if scenarios that take into account monthly savings, time horizons, and target amounts.Linked accounts for big picture planning

Our easy-to-use online platform links employee savings accounts, outside investments, IRAs—even spousal/partner assets—to create a real-time snapshot of their finances, making it easy for them to see the big picture. That means that in a single, holistic view, employees can track both their 401(k) plan account and their emergency fund.Personalized advice to help employees save for today (and someday)

By offering personalized advice, Betterment can help your employees make strides toward their long- and short-term financial goals. In fact, by using our automated tools and following our recommended investment advice, employees could earn 38% more money over 30 years compared with the average investor.

Ready for a better way to help your employees prepare for the inevitable—and the unexpected? Talk to Betterment today.

Help your employees prepare financially

Get started>