Amanda Bolan, like many of us, had a “pressure cooker” moment where she realized that becoming a real estate tycoon was part of her future. At the time, she was […]

Did you miss our previous article…

https://diyinvestorresources.com/?p=308

Amanda Bolan, like many of us, had a “pressure cooker” moment where she realized that becoming a real estate tycoon was part of her future. At the time, she was […]

Did you miss our previous article…

https://diyinvestorresources.com/?p=308

Many of you have been anxiously awaiting this information for several months, and it is finally here. We now have more insight into what the proposed tax policies and changes may look like.

Did you miss our previous article…

https://diyinvestorresources.com/?p=302

High-income earners have a better shot at retiring early than those making a median income. That being said, with more money comes more investing risk. After the great recession, Bob […]

Did you miss our previous article…

https://diyinvestorresources.com/?p=290

Designing a 401(k) plan is like building a house. It takes care, attention, and the help of a few skilled professionals to create a plan that works for both you and your employees. In fact, thoughtful plan design can help motivate even reluctant retirement savers to start investing for their future.

As you embark on the 401(k) design process, there are many options to consider. In this article, we’ll take you through the most important choices so you can make well-informed decisions. Since certain choices may not be available on the various pricing models of any given provider, make sure you understand your options and the trade-offs you’re making.

Let’s get started!

When would you like employees to be eligible to participate in the plan? You can opt to have employees become eligible:

Immediately – as soon as they begin working for your companyAfter a specific length of service – for example, a period of hours, months, or years of service

It’s also customary to have an age requirement (for example, employees must be 18 years or older to participate in the plan). Plus, you may want to add an “employee class exclusion” to prevent part-time, seasonal, or temporary employees from participating in the plan.

Once employees become eligible, they can immediately enroll – or, you can restrict enrollment to a monthly, quarterly, or semi-annual basis. If you have immediate 401(k) eligibility and enrollment, in theory, more employees could participate in the plan. However, if your company has a higher rate of turnover, you may want to consider adding service length requirements to alleviate the unnecessary administrative burden of having to maintain many small accounts of employees who are no longer with your organization.

Enrollment is another important feature to consider as you structure your plan. You may simply allow employees to enroll on their own, or you can add an automatic enrollment feature. Automatic enrollment (otherwise known as auto-enrollment) allows employers to automatically deduct elective deferrals from employees’ wages unless they elect not to contribute.

With automatic enrollment, all employees are enrolled in the plan at a specific contribution rate when they become eligible to participate in the plan. Employees have the freedom to opt out and change their contribution rate and investments at any time.

As you can imagine, automatic enrollment can have a significant impact on plan participation. In fact, according to research by The Pew Charitable Trusts, automatic enrollment 401(k) plans have participation rates greater than 90%! That’s in stark contrast to the roughly 50% participation rate for plans in which employees must actively opt in.

If you decide to elect automatic enrollment, consider your default contribution rate carefully. A 3% default contribution rate is still the most popular; however, more employers are electing higher default rates because research shows that opt-out rates don’t appreciably change even if the default rate is increased. Many financial experts recommend a savings rate of at least 10%, so using a higher automatic enrollment default rate gets employees even more of a head start.

You’re permitted to exclude certain types of compensation for plan purposes, including compensation earned prior to plan entry and fringe benefits for purposes of compliance testing and allocating employer contributions. You may choose to define your compensation as:

W2 (box 1 wages) plus deferrals – Total taxable wages, tips, prizes, and other compensation3401(a) wages – All wages taken into account for federal tax withholding purposes, plus the required additions to W-2 wages listed aboveSection 415 Safe Harbor – All compensation received from the employer which is includible in gross income

Want to encourage employees to enroll in the plan? Free money is a great place to start! That’s why more employers are offering profit sharing or matching contributions.

In fact, EBRI and Greenwald & Associates’ found that nearly 73% of workers said they were likely to save for retirement if their contributions were matched by their employer.

Some of the more common employer contributions are:

Safe harbor contributions – With the added bonus of being able to avoid certain time-consuming compliance tests, safe harbor contributions often follow one of these formulas:>Basic safe harbor match—Employer matches 100% of employee contributions, up to 3% of their compensation, plus 50% of the next 2% of their compensation.Enhanced safe harbor match—Employer matches 100% of employee contributions, up to 4% of their compensation.Non-elective contribution—Employer contributes 3% of each employee’s compensation, regardless of whether they make their own contributions.Discretionary matching contributions – You decide what percentage of employee 401(k) deferrals to match and the maximum percentage of pay to match. For example, you could elect to match 50% of contributions on up to 6% of compensation. One advantage of having a discretionary matching contribution is that you retain the flexibility to adjust the matching rate as your business needs change.Non-elective contributions – Each pay period, you have the option of contributing to your employees’ 401(k) accounts, regardless of whether they contribute. For example, you could make a profit sharing contribution (one type of non-elective contribution) at the end of the year as a percentage of employees’ salaries or as a lump-sum amount.

In addition to helping your employees build their retirement nest eggs, employer contributions are also tax deductible (up to 25% of total eligible compensation), so it may cost less than you think. Plus, offering an employer contribution can play a key role in recruiting and retaining top employees. In fact, a Betterment for Business study found that more than 45% of respondents considered a 401(k) match to be a factor when deciding whether to accept a job.

If you elect to make an employer contribution, you also need to decide on a vesting schedule (an employee’s own contributions are always 100% vested). Note that all employer contributions made as part of a safe harbor plan are immediately and 100% vested.

The three main vesting schedules are:

Immediate – Employees are immediately vested in (or own) 100% of employer contributions as soon as they receive them.Graded – Vesting takes place in a gradual manner. For example, a six-year graded schedule could have employees vest at a rate of 20% a year until they are fully vested.Cliff – The entire employer contribution becomes 100% vested all at once, after a specific period of time. For example, if you had a three-year cliff vesting schedule and an employee left after two years, they would not be able to take any of the employer contributions (only their own).

Like your eligibility and enrollment decisions, vesting can also have an impact on employee participation. Immediate vesting may give employees an added incentive to participate in the plan. On the other hand, a longer vesting schedule could encourage employees to remain at your company for a longer time.

If you decide to use length of service to determine your eligibility and vesting schedules, you must also decide how to measure it. Typically, you may use:

Elapsed time – Period of service as long as employee is employed at the end of periodActual hours – Actual hours worked. With this method, you’ll need to track and report employee hoursActual hours/equivalency – A formula that credits employees with set number of hours per pay period (for example, monthly = 190 hours)

Naturally, there will be times when your employees need to withdraw money from their retirement accounts. Your plan design will have rules outlining the withdrawal parameters for:

TerminationIn-service withdrawals (at attainment of age 59 ½; rollovers at any time)HardshipsQualified Domestic Relations Orders (QDROs)Required Minimum Distributions (RMDs)

Plus, you’ll have to decide whether to allow participants to take 401(k) plan loans (and the maximum amount of the loan). While loans have the potential to derail employees’ retirement dreams, having a loan provision means employees can access their money if they need it and employees can pay themselves back plus interest. If employees are reluctant to participate because they’re afraid their savings will be “locked up,” then a loan provision can help alleviate that fear.

When it comes to investment methodology, there are many strategies to consider. Your plan provider can help guide you through the choices and associated fees. For example, at Betterment, we believe that ETFs offer investors significant diversification and flexibility at a low cost. Plus, we offer ETFs in conjunction with personalized, unbiased advice to help today’s retirement savers pursue their goals.

Your 401(k) plan provider can walk you through your plan design choices and help you tailor a plan that works for your company and your employees. Once you’ve settled on your plan design, you will need to codify those features in the form of a formal plan document to govern your 401(k) plan. At Betterment, we draft the plan document for you and provide it to you for review and final approval.

Your business is likely to evolve—and your plan design can evolve, too. Drastic increase in profits? Consider adding an employer match or profit sharing contribution to share the wealth. Plan participation stagnating? Consider adding an automatic enrollment feature to get more employees involved. Employees concerned about access to their money in an uncertain world? Consider adding a 401(k) loan feature.

Need a little help figuring out your plan design? Talk to Betterment. Our experts make it easy for you to offer your employees a better 401(k) quickly and easily—all for a fraction of the cost of most providers.

Want a better 401(k)?

Learn More>

Did you miss our previous article…

https://diyinvestorresources.com/?p=218

Financial freedom is attainable for all of us, but how fast we reach it differs greatly. You may be making $100 profit per month on each single-family home you buy, […]

Did you miss our previous article…

https://diyinvestorresources.com/?p=209

If you ran your IPS through a stress test, would it be strong enough to withstand the pressure?

Did you miss our previous article…

https://diyinvestorresources.com/?p=196

You hear Brandon Turner’s voice quite often on the BiggerPockets Real Estate Podcast, but rarely is it heard advising new investors. Today, Brandon is taking on three live “coaching calls” […]

Did you miss our previous article…

https://diyinvestorresources.com/?p=192

Creative financing allows investors to quickly grow their portfolio and invest in properties traditional lenders won’t touch. Here are the power tools you need to win with creative financing.

Did you miss our previous article…

https://diyinvestorresources.com/?p=191

Your home may be the largest single purchase you make during your lifetime. That can make it both incredibly exciting and nerve wracking.

Purchasing a primary residence often falls in the grey area between a pure investment (meant to increase one’s capital) and a consumer good (meant to increase one’s satisfaction). Your home has aspects of both, and we recognize that you may purchase a home for reasons that are not strictly monetary, such as being in a particular school district or proximity to one’s family. Those are perfectly valid inputs to your purchasing decision.

However, as your financial advisor, this guide will focus primarily on the financial aspects of your potential home purchase: We’ll do this by walking through the five tasks that should be done before you purchase your home.

Houses are built on top of foundations to help keep them stable. Just like houses, your finances also need a stable foundation. Part of that includes your emergency fund. We recommend that, before purchasing a home, you should have a fully-funded emergency fund. Your emergency fund should be a minimum of three months’ worth of expenses.

How big your emergency fund should be is a common question. By definition, emergencies are difficult to plan for. We don’t know when they will occur or how much they will cost. But we do know that life doesn’t always go smoothly, and thus that we should plan ahead for unexpected emergencies.

Emergency funds are important for everyone, but especially so if you are a homeowner. When you are a renter, your landlord is likely responsible for the majority of repairs and maintenance of your building. As a homeowner, that responsibility now falls on your shoulders. Yes, owning a home can be a good investment, but it can also be an expensive endeavor. That is exactly why you should not purchase a home before having a fully-funded emergency fund.

And don’t forget that your monthly expenses may increase once you purchase your new home. To determine the appropriate size for your emergency fund, we recommend using what your monthly expenses will be after you own your new home, not just what they are today.

Open your Safety Net

Get Started>

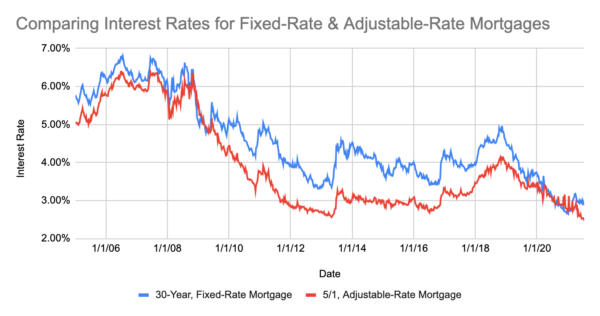

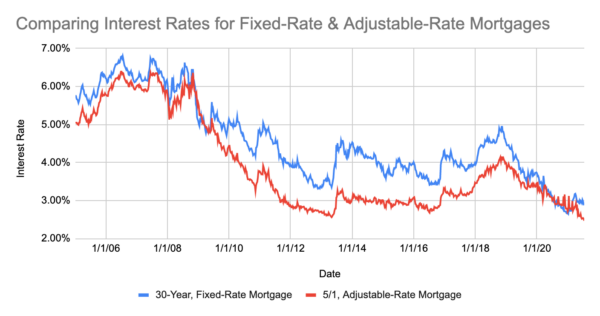

According to 2020 survey data by the National Association of Realtors®, 86% of home buyers took out a mortgage. This means that most people have to choose which type of mortgage is appropriate for them, and one of the key factors is deciding between an adjustable-rate mortgage (ARM) and a fixed-rate mortgage (FRM). Betterment generally recommends choosing a fixed-rate mortgage.

Here’s why:

As shown below, ARMs usually—but not always—offer a lower initial interest rate than FRMs.

Source: Federal Reserve Bank of St. Louis. Visualization of data by Betterment.

But this lower rate comes with additional risk. With an ARM, your monthly payment can increase over time, and it is difficult to predict what those payments will be. This may make it tough to stick to a budget and plan for your other financial goals.

Fixed-rate mortgages, on the other hand, lock in the interest rate for the lifetime of the loan. This stability makes budgeting and planning for your financial future much easier. Locking in an interest rate for the duration of your mortgage helps you budget and minimizes risk.

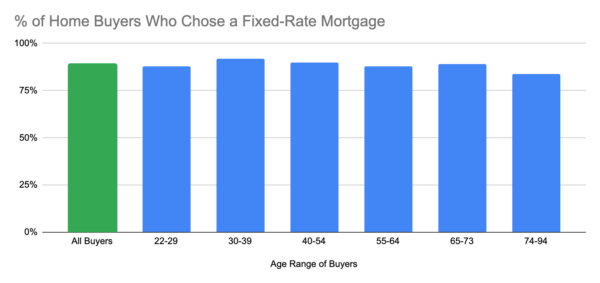

Luckily, most home buyers do choose a fixed-rate mortgage. According to 2020 survey data by the National Association of Realtors®, 89% of home buyers who financed their home purchase used a fixed-rate mortgage, and this was very consistent across all age groups. Research by the Urban Institute also shows FRMs have accounted for the vast majority of mortgages over the past 2 decades.

Source: National Association of Realtors®, 2020 Home Buyers and Sellers Generational Trends. Visualization of data by Betterment.

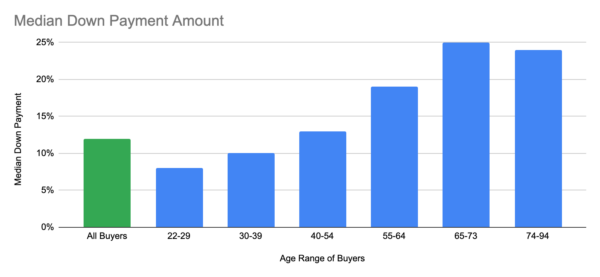

You’ll need more than just your emergency fund to purchase your dream home. You’ll also need a down payment and money for closing costs. Betterment recommends making a down payment of at least 20%, and setting aside about 2% of the home purchase for closing costs.

A 2020 National Association of Realtors® survey shows the median down payment amount for home purchases is 12%. As the chart below shows, younger buyers tend to make smaller down payments than older buyers.

Source: National Association of Realtors®, 2020 Home Buyers and Sellers Generational Trends. Visualization of data by Betterment.

But is making an average down payment of only 12% a wise decision? It is true that you are often allowed to purchase a home with down payments far below 20%. For example:

FHA loans allow down payments as small as 3.5%.Fannie Mae allows mortgages with down payments as small as 3%.VA loans allow you to purchase a home with no down payment.

However, Betterment typically advises putting down at least 20% when purchasing your home. A down payment of 20% or more can help avoid Private Mortgage Insurance (PMI). Putting at least 20% down is also a good sign you are not overleveraging yourself.

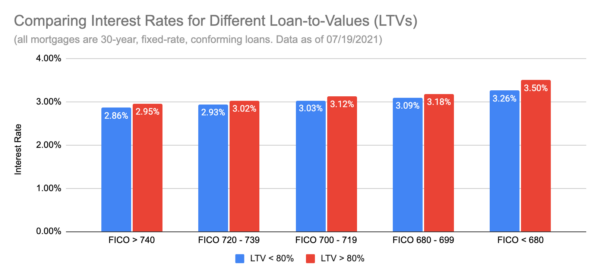

Lastly, a down payment of at least 20% may help lower your interest rate. This is acknowledged by the CFPB and seems to be true when we compare interest rates of mortgages with Loan-to-Values (LTVs) below and above 80%, as shown below.

Source: Federal Reserve Bank of St. Louis. Visualization of data by Betterment.

Depending on your situation, it may even make sense to go above a 20% down payment. Just remember, you shouldn’t put every spare dollar you have into your home, as that will likely mean you don’t have enough liquid assets elsewhere for things such as your emergency fund and other financial goals like retirement.

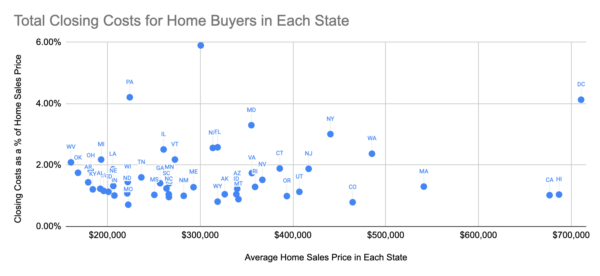

In addition to a down payment, buying a home also has significant transaction costs. These transaction costs are commonly referred to as “closing costs” or “settlement costs.”

Closing costs depend on many factors, such as where you live and the price of the home.

ClosingCorp, a company that specializes in closing costs and services, conducted a study that analyzed 2.9 million home purchases throughout 2020. They found that closing costs for buyers averaged 1.69% of the home’s purchase price, and ranged between states from a low of 0.71% of the home price (Missouri) up to a high of 5.90% of the home price (Delaware). The chart below shows more detail.

Source: ClosingCorp, 2020 Closing Cost Trends. Visualization of data by Betterment.

As a starting point, we recommend saving up about 2% of the home price (about the national average) for closing costs. But of course, if your state tends to be much higher or lower than that, you should plan accordingly.

In total, that means that you should generally save at least 20% of the home price to go towards a down payment, and around 2% for estimated closing costs.

With Betterment, you can open a Major Purchase goal and save for your downpayment and closing costs using either a cash portfolio or investing portfolio, depending on your risk tolerance and when you think you’ll buy your home.

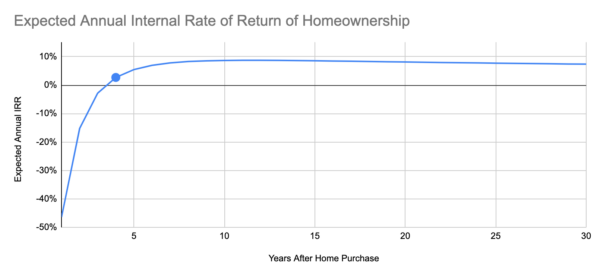

We mentioned the closing costs for buyers above, but remember: There are also closing costs when you sell your home. These closing costs mean it may take you a while to break even on your purchase, and that selling your home soon after is more likely to result in a financial loss. That’s why Betterment doesn’t recommend buying a home unless you plan to own that home for at least 4 years, and ideally longer.

Unfortunately, closing costs for selling your home tend to be even higher than when you buy a home. Zillow, Bankrate, NerdWallet, The Balance and Opendoor all estimate them at around 8% to 10% of the home price.

Betterment’s research analyzed closing costs for both buying and selling, the opportunity costs of potentially investing that money, and more. It shows that the average expected breakeven time is about 4 years as shown below. Of course, this will depend on many factors, but is helpful as a general guide. Thus, if you do not plan to own your home for at least 4 years, you should think carefully on whether buying a home is a smart move at this point in your life.

Source: Betterment, Is Buying A Home A Good Investment? Visualization of data by Betterment.

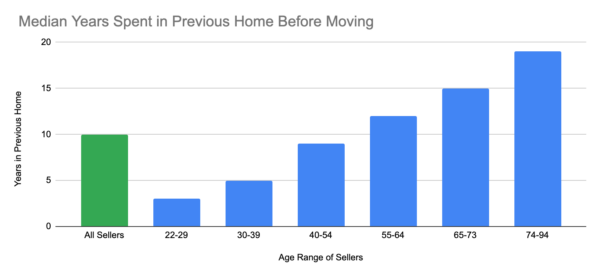

Luckily, it appears that most home buyers stay in their homes beyond our 4-year rule of thumb. The chart below is built from 2020 survey data by the National Association of Realtors®. It shows how long individuals of various age groups stayed in their previous homes before selling them.

Across all age groups, the median length of time was 10 years, which is more than double our 4-year rule of thumb. That’s excellent. However, we can see that younger buyers, on average, come in well below the 10-year median, which indicates they are more at risk of not breaking even on their home purchases.

Source: National Association of Realtors®, 2020 Home Buyers and Sellers Generational Trends. Visualization of data by Betterment.

Some things you can do to help ensure you stay in your home long enough to at least break even include:

If you’re buying a home in an area you don’t know very well, consider renting in the neighborhood first to make sure you actually enjoy living there.Think ahead and make sure the home makes sense for you 4 years from now, not just you today. Are you planning on having kids soon? Might your elderly parents move in with you? How stable is your job? All of these are good questions to consider.Don’t rush your home purchase. Take your time and think through this very large decision. The phrase “measure twice, cut once” is very applicable to home purchases.

The upfront costs are just one component of home affordability. The other is the ongoing monthly costs. Betterment recommends building a financial plan to determine how much home you can afford while still achieving your other financial goals. But if you don’t have a financial plan, we recommend not exceeding a debt-to-income (DTI) ratio of 36%.

In other words, you take your monthly debt payments (including your housing costs), and divide them by your gross monthly income. Lenders often use this as one factor when it comes to approving you for a mortgage.

There are lots of rules in terms of what counts as income and what counts as debt. These rules are all outlined in parts of Fannie Mae’s Selling Guide and Freddie Mac’s Seller/Servicer Guide. While the above formula is just an estimate, it is helpful for planning purposes.

In certain cases Fannie Mae and Freddie Mac will allow debt-to-income ratios as high as 45%-50%. But just because you can get approved for that, doesn’t mean it makes financial sense to do so.

Keep in mind that the lender’s concern is your ability to repay the money they lent you. They are far less concerned with whether or not you can also afford to retire or send your kids to college. The debt to income ratio calculation also doesn’t factor in income taxes or home repairs, both of which can be significant.

This is all to say that using DTI ratios to calculate home affordability may be an okay starting point, but they fail to capture many key inputs for calculating how much you personally can afford. We’ll outline our preferred alternative below, but if you do choose to use a DTI ratio, we recommend using a maximum of 36%. That means all of your debts—including your housing payment—should not exceed 36% of your gross income.

In our opinion, the best way to determine how much home you can afford is to build a financial plan. That way, you can identify your various financial goals, and calculate how much you need to be saving on a regular basis to achieve those goals. With the confidence that your other goals are on-track, any excess cash flow can be used towards monthly housing costs. Think of this as starting with your financial goals, and then backing into home affordability, instead of the other way around.

If owning a home is important to you, you can use the five steps in this guide to help you make a wiser purchasing decision.

Have an emergency fund of at least three months’ worth of expenses to help with unexpected maintenance and emergencies.Choose a fixed-rate mortgage to help keep your budget stable.Save for a minimum 20% down payment to avoid PMI, and plan for paying ~2% in closing costs.Don’t buy a home unless you plan to own it for at least 4 years. Otherwise, you are not likely to break even after you factor in the various costs of homeownership.Build a financial plan to determine your monthly affordability, but as a starting point, don’t exceed a debt-to-income ratio of 36%.

If you’d like help saving towards a down payment or building a financial plan, sign up for Betterment today.

Save for your home with Betterment

Get Started>

Did you miss our previous article…

https://diyinvestorresources.com/?p=166

Finding a good deal in the current real estate market can be pretty difficult. Prices are maxed out in most markets and sellers are getting bombarded by offers, many of […]

Did you miss our previous article…

https://diyinvestorresources.com/?p=152